With inflation currently running at just above 6%, its highest level since 1990, and especially since it got there so rapidly (the annual rate was 1.68% in February of this year, as the economy continued its recovery from the pandemic doldrums), many investors are starting to worry about increases in the cost of living and how a higher rate of inflation will affect the economy and their investments.

Investors aren’t alone in their inflation concerns. Recently, Fed Chair Jerome Powell announced the US central bank’s plans to scale back bond purchases, which have been a major source of the waves of liquidity pumped into the US economy in order to maintain equilibrium in the face of the pandemic shutdown. The Fed, along with the central banks of other nations, uses several tools in its efforts to keep long-term inflation in or near what is sometimes called the “Goldilocks Zone”: around 2%.

Some inflation is actually considered healthy for an economy, since it encourages consumers to spend their money today, when it has a bit more purchasing power, rather than hoarding cash, which restricts the flow of currency and can actually be harmful to the economy. But too much inflation can wreck an economy, as happened in Germany after World War I, and more recently in places like Venezuela, where disastrous hyperinflation has caused increases in the cost of goods and services on the order of a million percent per month.

So, as inflation ramps up during the current economic expansion, investors, analysts, and policymakers are keeping a close eye on developments. Though the equity markets have been in an almost unparalleled state of expansion since their lows during the early days of the pandemic, recently we have observed pullbacks in response to inflationary trends in the economy, such as rising prices for basic consumer goods. While Fed Chair Powell and other analysts insist that the current rate of inflation is a cause for caution and not alarm, other observers worry that the inflation cat is already out of the bag and will pose challenges for the economy’s continued expansion.

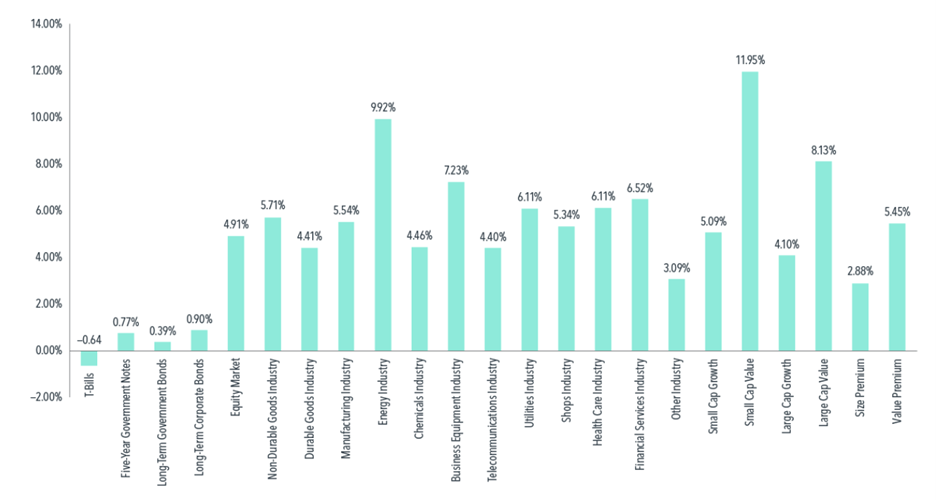

What should investors do? At present, it seems that the best course may be to remain diversified and stick with established long-range investment strategies. As the chart indicates, historical data suggest that over the long haul, portfolios that are well-diversified among various asset classes have tended to maintain growth rates that generally protect assets from the long-term erosion in purchasing power caused by inflation. A recent study of the period 1927–2020, for example, during times when inflation was running above the median range of about 5.5%, investments in various types of equities, as well as medium- and long-term Treasuries, provided returns in excess of inflation. This may suggest that one of the best inflation hedges for portfolios is simply to remain invested according to a long-term plan.

As always if you wish to discuss this topic further, please feel free to reach out to our office

SOURCE: Dimensional Fund Advisors. Past performance is no guarantee of future results; indexes are not available for direct investment.

SOURCES:

1. “US Inflation Rate, 1960–2021,” Macrotrends.net, https://www.macrotrends.net/countries/USA/united-states/inflation-rate-cpi

2. Saphir, Marte, and Dunsmuir, “Fed Lays Out Plan to Reduce Bond Purchases, Flags Inflation Worries,” Reuters.com, Octdober 13, 2021, https://www.reuters.com/business/patient-or-aggressive-fed-policymakers-split-inflation-response-2021-10-13/

3. John Schmidt, “How Inflation Erodes the Value of Your Money,” Forbes.com, May 3, 2021, https://www.forbes.com/advisor/investing/what-is-inflation/

4. Brittany De Lea, “Fed’s Powell Says All Americans Will Have Job Opportunities as Economy Recovers,” June 17, 2021, FoxBusiness.com, https://www.foxbusiness.com/economy/fed-powell-americans-want-to-work-again

5. Mohammed A. El-Erian, “Opinion: The Fed Continues to Fall behind the Curve,” Bloomberg.com, June 20, 2021, https://www.bloombergquint.com/opinion/federal-reserve-meeting-central-bank-continues-to-fall-behind-curve